Frequently Asked Questions (FAQs)

Below are FAQs, or links to FAQs, developed in the course of a number of capital markets industry projects.

Foire aux questions (FAQ)

Voici les FAQ, ou liens vers des FAQ, développées au cours de plusieurs projets dans l’industrie des marchés financiers.

Below you will find the questions and answers developed for the move from a T+2 to a T+1 securities settlement cycle, with more recent FAQs added at the top. Additionally, a good number of the CCMA’s T+3-to-T+2 FAQs may also be useful at some point. Please also check out U.S. T+1 FAQs.

Les questions et réponses formulées en vue du passage éventuel d’un cycle de règlement des opérations sur titres de T+2 à T+1 sont présentées ici, les questions les plus récentes figurant en haut de page. Un bon nombre des points de la FAQ T+3 à T+2 de l’ACMC seront également utiles occasionnellement. Consultez également les FAQ T+1 américaines.

29. What should issuers and their securities lawyers and other advisors know about moving to a shorter settlement cycle?

Issuers and their advisors may have heard something about a shorter trade settlement cycle but they should know that there is an impact for them also. They should know that the number of days it takes to settle a trade in secondary markets in North America is reducing from the current two business days after a trade (T+2) to next day – T+1 – effective May 27, 2024 in Canada and Mexico, and May 28, 2024 in the U.S. (May 27 being a U.S. holiday). While primary markets are out of scope of the change, related corporate actions may be affected. Because the change from T+2 to T+1 settlement is more complex than the T+3 to T+2 transition, issuers and their advisors are encouraged to:

- Avoid creating new events that settle on either the first date set for trading on a T+1 basis (May 27) or the May 28 ‘double settlement’ date when trades from two business days prior (the last day of T+2 trading) as well as May 27 – the first day of T+1 trading – will settle on the same day.

- Have staff ready to address questions that may arise during transition.

- Consider appropriate internal and external communications for stakeholders.

Background:

Corporate action events involve the calculation and payment to a securities holder of cash and/or securities, whether mandatory (e.g., interest, dividends, principal repayment at maturity) – when beneficial holders will receive the entitlement without having to make a decision – or voluntary, when beneficial holders must decide to accept or ignore an offer (e.g., rights subscriptions, tenders). Corporate actions include: (i) events that affect corporate share or debt structure or payments, such as corporate reorganizations (e.g., mergers or acquisitions, leveraged buy-outs or tender offers), (ii) special stock transactions (e.g., splits, rights offerings, conversions, odd lot programs), and (iii) changes in capital structure (e.g., through flotations, mergers, takeovers or capital reorganizations).

Effect of the move to T+1 on entitlements:

| Function | Current Practice | Practice as of May 27, 2024 |

| Distribution Events

if base security trades… |

· Without due bills:[1] ex-date is record date minus 1

· With due bills: ex-date is the due bill redemption date minus 1 |

· Without due bills: ex-date is record date

· With due bills: ex-date is due bill redemption date |

| Mandatory Events | · CDS payable date is delisting date plus 3 | · CDS payable date is delisting date plus 2 |

| Mandatory with Options Events

Event set-up is date-driven, not driven by the settlement period |

· CNS restriction and trade conversion dates are calculated based on the agent expiry and payable dates provided by external sources | · No changes |

| Voluntary Events

(Letter of guaranteed delivery for event expiries (cover/protect period)[2]) |

· Expiry date plus 2 | · Expiry date plus 1 |

Transition:

Changes to the TSX Company Manual related to T+1 settlement will be effective May 27, 2024. Other dates relevant to the change in ex-date calculation of corporate action events are as follows (with U.S. equivalents added for convenience).

| Record Date | Ex Date (Canada) | Ex Date (U.S.) |

| Friday, May 24, 2024

(last day of trading for T+2 settlement) |

Thursday, May 23, 2024 | Same as Canada |

| Monday, May 27, 2024

(first day of trading for T+1 settlement) |

Monday, May 27, 2024 | Closed |

| Tuesday, May 28, 2024 | Tuesday, May 28, 2024 | Same as Canada |

| Wednesday, May 29, 2024 | Wednesday, May 29, 2024 | Same as Canada |

[1] An exchange may set a later ex-date (e.g., because of challenges with stock or large cash dividends) and relevant securities will trade with a ‘due bill’ attached and have a non-standard ex-date.

[2] Investors can purchase securities even on the offer’s expiration date, with the protect feature ‘covered’ once the securities settle.

29. Quelles actions doivent prendre les émetteurs, leurs avocats spécialisés en valeurs mobilières et leurs autres conseillers pour la transition à un cycle de règlement plus court?

Les émetteurs et leurs conseillers ont peut-être eu vent d’un cycle de règlement des transactions plus court, dont ils connaissent l’incidence. Ils devraient savoir que le nombre de jours nécessaires pour le règlement d’une transaction sur les marchés secondaires nord-américains passe de deux jours ouvrables après la transaction (T+2) au jour suivant (T+1) dès le 27 mai 2024 au Canada et au Mexique, et le 28 mai 2024 aux États-Unis (le 27 mai étant un jour férié aux États-Unis). Les marchés primaires ne sont pas visés par cette modification, mais les droits connexes sont susceptibles de l’être. Le passage du règlement T+2 à T+1 s’avère plus complexe que le passage de T+3 à T+2, aussi, les émetteurs et leurs conseillers sont invités à :

- Éviter de créer de nouveaux événements dont le dénouement a lieu soit à la première date fixée pour la négociation à T+1 (27 mai), soit à la date de « double règlement » du 28 mai, lorsque les transactions effectuées deux jours ouvrables précédemment (dernier jour de négociation T+2) ainsi que le 27 mai — premier jour de la négociation T+1 — se dénoueront le même jour.

- Préparer les effectifs à répondre aux questions posées durant la transition.

- Envisager des communications internes et externes appropriées pour leurs parties prenantes.

Contexte :

Les événements de marché impliquent le calcul et le paiement à un détenteur de titres de liquidités et/ou de titres, obligatoires (par exemple, intérêts, dividendes, remboursement du capital à la date d’échéance) — lorsque les bénéficiaires réels recevront le droit sans prendre de décision — ou volontaires, lorsque les bénéficiaires réels devront accepter ou ignorer une offre (par exemple, souscription de droits, appels d’offres). Les événements de marché englobent (i) ceux qui touchent la structure des actions ou de la dette de la société ou les paiements, comme les réorganisations de sociétés (par exemple, fusions ou acquisitions, rachats de sociétés par effet de levier ou offres publiques d’achat), (ii) les transactions spéciales sur actions (par exemple, fractionnements, offres de droits, conversions, programmes de lots irréguliers), et (iii) les modifications à la structure du capital (par exemple, via l’introduction en bourse, fusions, acquisitions ou réorganisations du capital).

Effet du passage à T+1 sur les droits :

| Évènement | Pratique actuelle | Pratique au 27 mai 2024 |

| Événements de distributions

Si le titre de base est échangé… |

· Sans factures exigibles:[1] date d’échéance est la date d’enregistrement moins 1

· Avec des factures exigibles : la date ex est la date de remboursement de la facture exigible moins 1 |

· Sans factures exigibles : la date ex est la date d’enregistrement

· Avec factures exigibles : la date ex est la date de remboursement des factures exigibles |

| Événements obligatoires

|

· La date de paiement du CDS est la date de radiation de la cote plus 3 | · La date de paiement du CDS est la date de radiation de la cote plus 2 |

| Obligatoire avec les événements d’options

La mise en place de l’événement est déterminée par la date et non par la période de règlement. |

· Les dates de restriction de la SNC et de conversion commerciale sont calculées sur la base des dates d’échéance et d’exigibilité de l’agent fournies par des sources externes. | · Pas de changement |

| Événements volontaires

Lettre de garantie de livraison pour les échéances de l’événement (période de couverture/protection)[2] |

· Date d’échéance plus 2 | · Date d’échéance plus 1 |

Transition:

Les changements apportés au Guide de la TSX à l’intention des sociétés relativement au règlement à T+1 entreront en vigueur le 27 mai 2024. Les autres dates relatives au changement de calcul de la date ex-date des opérations sur titres sont les suivantes (les équivalents américains sont ajoutés pour raisons de commodité).

| Date d’enregistrement | Date d’échéance (Canada) | Date d’échéance (U.S.) |

| Vendredi 24 mai 2024

(dernier jour de négociation pour le règlement T+2) |

Jeudi 23 mai 2024 | Même chose qu’au Canada |

| Lundi 27 mai 2024

(premier jour de négociation pour le règlement à T+1) |

Lundi 27 mai 2024 | Fermé |

| Mardi 28 mai 2024 | Mardi 28 mai 2024 | Même chose qu’au Canada |

| Mercredi 29 mai 2024 | Mercredi 29 mai 2024 | Même chose qu’au Canada |

[1] Une bourse peut fixer une date d’expiration plus tardive (par exemple, en raison de problèmes liés à des actions ou à des dividendes en espèces importants) et les titres concernés seront négociés avec une « facture exigible » et auront une date d’expiration non standard.

[2] Les investisseurs peuvent acquérir des titres même à la date d’expiration de l’offre, la fonction de protection étant « couverte » une fois les titres réglés.

28. Do CIRO-registered Dealers currently – and will they after the updated CIRO T+1 rule changes are in effect – have to submit exception reports to CIRO if the 90% matching requirements aren’t met? (September 29, 2023)

Under current CIRO rules, an exception report must be filed with CIRO if the broker-to-broker quarterly compliant trade percentage is less than 90%. Dealers must continue to file exception reports with CIRO until the proposed rule amendments are implemented (targeted for before the May 27, 2024 T+1 Canadian implementation date).

Once the new rules are in place, Dealers will no longer be required to file an exception report with CIRO even if the quarterly compliant trade percentage is less than 90%. However, CIRO will continue to monitor Dealers’ trade-matching percentages each quarter. Based on firm-by-firm data received from CDS, CIRO may request an action plan, explanation, or other information if a Dealer’s trade percentage is consistently or significantly below 90%.

28. Les courtiers inscrits auprès de l’OCRI doivent-ils, présentement et suite à l’entrée en vigueur des modifications à la règle T+1 de l’OCRI, soumettre des rapports d’exception à l’OCRI en cas de non-respect des exigences d’appariement de 90 %? (29 septembre 2023)

Conformément aux règles actuelles de l’OCRI un rapport d’exception doit être produit auprès de l’OCRI si le pourcentage de transactions trimestrielles conformes de courtier à courtier est moindre que 90 %. Les courtiers continueront à produire des rapports d’exception auprès de l’OCRI jusqu’à la date de mise en œuvre des modifications de règles proposées (avant le 27 mai 2024, date de mise en œuvre canadienne T+1).

Dès que les nouvelles règles seront en vigueur, les courtiers n’auront plus l’obligation de produire un rapport d’exception auprès de l’OCRI, même si le pourcentage trimestriel de transactions conformes est inférieur à 90 %. Cependant, l’OCRI continuera de surveiller les pourcentages d’appariement des transactions de courtiers, chaque trimestre. Selon les données de chaque société reçues de la CDS, l’OCRI pourra demander un plan d’action, un justificatif ou d’autres informations si le pourcentage de transactions d’un courtier est régulièrement ou très inférieur à 90 %.

27. Is there a consensus on securities loan recall times with the change to T+1? (September 29, 2023)

SIFMA (Securities Industry and Financial Markets Association), the Canadian Securities Lending Association (CASLA), and the Risk Management Association (RMA) met in the summer of 2023 to discuss an acceptable date and time for recalls in a T+1 environment. While securities lending agreements can reflect a specific recall time negotiated by a lender and borrower, the timing of recalls generally defaults to what is in standard securities lending agreements – usually a master securities lending agreement (MSLA) or global agreement (GMSLA) – which use language that defaults to a cut-off of close of business or market practice.

In today’s T+2 settlement cycle, close of business is understood to be market close, and market practice for a recall is 3 p.m. ET on T+2 in the U.S. and Canada. While the SIFMA T+1 Playbook, based on U.S. industry input, identified market “best practice” as moving from 3 p.m. on T+1 to 11:59 p.m. on T for a “T” recall, most legal agreements refer simply to “close of business” or “market practice:” a 3 p.m. cut-off will not change and as of May 27, 2024 will constitute an “effective T recall.” With a 3:00 p.m. ET on T cut-off, borrowers will have at least the last hour of the trading day to process the recall and/or determine if they need to buy the securities back.

To enforce a later (11:59 p.m.) on T cut-off, legal agreements between the borrower and lender would need to be amended. While agent lenders might like to have until 11:59 p.m. to issue a “T” recall (and might be prepared to make the necessary effort to amend agreements to achieve this), it is believed to be unlikely that borrowers would agree to such a change because they do not have the ability after the close of business on T to settle securities, source additional supply, or purchase securities if needed.

The majority of market participants are understood to be onside with 3 p.m. on T recalls. Moreover, the TMX portal should help streamline the recall process so that more recalls can be entered before the cut-off. Even recalls entered after a 3 p.m. cut-off on T will have benefits as the related automation will alert global desks of the pending recall, so they can try to source additional supply, whether it’s in the Far East, Europe or elsewhere. Worst-case scenario, notice of the recall will be available first thing on T+1, allowing an earlier start to finding alternative sources if needed.

27. Y a-t'il un consensus sur les délais de rappel de prêts de titres suite à la modification à T+1? (29 septembre 2023)

La Securities Industry and Financial Markets Association (SIFMA), l’Association canadienne de prêteurs de titres (CASLA) et la Risk Management Association (RMA) se sont réunies cet été 2023 pour se pencher sur une date et une heure acceptables pour les rappels en contexte T+1. Si les ententes afférentes aux prêts sur titres prévoient un délai de rappel spécifique que le prêteur et l’emprunteur négocient, le délai de rappel est fixé par défaut, habituellement, dans les ententes standard de prêt sur titres – entente-cadre de prêt sur titres (ECPT) ou une entente-cadre globale de prêt sur titres (ECGPT) – prévoyant par défaut une date limite de clôture des transactions ou des pratiques de marché.

Quant au cycle de règlement T+2 actuel, la clôture des transactions est réputée être la clôture du marché, et la pratique du marché pour un rappel est fixée à 15 h (heure de l’Est) à T+2 aux États-Unis et au Canada. Toutefois, le guide T+1 de la SIFMA, selon les commentaires du secteur américain, indique que la « meilleure pratique » du marché est de passer de 15 h le jour T+1 à 23 h 59 le T pour un rappel « T », la plupart des ententes légales font simplement référence à la « clôture des transactions » ou à la « pratique du marché » : la date limite de 15 h ne sera pas sujette à modifications et à partir du 27 mai 2024, constituera un « rappel T effectif ». Si l’heure limite est établie à 15 h le T, les emprunteurs disposeront au minimum de la dernière heure de la journée de négociation pour traiter le rappel et/ou déterminer le besoin de rachat de titres.

L’application d’une date limite plus tardive (23 h 59 le T) implique de modifier les ententes légales entre emprunteurs et prêteurs. Les prêteurs souhaiteront disposer jusqu’à 23 h 59 pour l’émission d’un rappel « T » (et seraient prêts à déployer des efforts pour modifier les ententes à cet effet), mais il est peu probable que les emprunteurs acquiescent à une telle modification, car il ne leur est pas possible, à la clôture du jour T, de régler les titres, de procéder à l’achat de produits supplémentaires ou de titres, si nécessaire.

Les participants au marché, dans leur grande majorité, sont unanimes pour effectuer les rappels à 15 h le T. Le portail TMX devrait en outre favoriser la rationalisation du processus de rappel; ainsi, davantage de rappels seront inscrits avant l’heure limite. Les rappels effectués après l’heure limite de 15 h le T présenteront tout de même des avantages, du fait de l’automatisation connexe notifiant les bureaux internationaux du rappel en cours, dans l’objectif de trouver des sources d’achat supplémentaires, en Extrême-Orient, en Europe ou d’autres régions du monde. Dans le moins favorable des scénarios, l’avis de rappel sera lancé dès la première heure le jour T+1, afin de rechercher plus tôt d’autres sources d’achat le cas échéant.

26. Are there T+1 changes to consider with respect to derivatives products (documentation, processing, transactions ‘in-flight,’ where agreements span May 27, 2024, etc.)? (September 29, 2023)

Are U.S. derivatives moving to T+1?

Yes, no, and maybe. If a derivative is DTC-eligible and there is otherwise no exemption, then it will move to T+1. Section 3(a)(10) of the Exchange Act includes security-based swaps and options, and excludes an exempted security (indeed, security-based swaps are exempted). Even if a derivative were exempt, it still may move to T+1 by agreement or market practice. For example, over-the-counter (OTC) options are not mandated to follow T+1, but are expected to align with listed options, which must move to T+1.

What derivatives will move to T+1?

At a SIFMA-hosted T+1 presentation by ISDA representatives, participants heard that, as a rule of thumb, firms could expect depository-eligible securities that moved from T+3 to T+2 to likely move from T+2 to T+1 to keep cash flows aligned (avoiding increased capital, pre-funding, or credit costs) and to reduce business risk between the derivative and corresponding hedge transaction as much as possible. The OTC market will follow suit to keep cash flows aligned as much as possible, and to avoid basis risk between securities and the related derivative instruments. Even for formal exceptions to the T+1 rule (for example, security-based swaps, which have been exempted), many parties may still choose to adopt T+1 to avoid mismatched settlement cycles.

- Equity derivatives are expected to be most impacted by T+1 while classes like credit derivatives are not expected to be impacted by T+1. Other asset classes may be affected to a greater or lesser extent and there may be further discussions among market participants. For example, ISDA equity working groups could discuss exotic/highly structured derivatives, including non-standard non-linear transaction types (e.g., barrier and compound options).

- Other asset classes that may be affected to some extent are those where a market participant may want to align payment dates of an interest rate swap with the settlement of the security. In the case of U.S. dollar for SOFR trading (Secured Overnight Financing Rate, a benchmark rate chosen to replace USD LIBOR), the derivatives convention is ‘compounded in arrears.’ SOFR is published on T+1, with the last observation made on the termination date when payment is due, providing little to no notice of the amount of interest due. Fortunately, there are new ISDA lookback, observation shift, and lockout conventions that have now been in place for several years. They are reflected in industry documentation, which has been deployed and is in use by the market. These allow observation of a rate so that the interest amount can be determined ahead of the payment date, allowing for certainty as to the amount and time to make that payment on T+1. Firms also may elect not to alter the observation of the rate, but to apply instead a payment delay to the floating amount, agreed on a trade-by-trade basis.

Will there be changes to derivatives documentation, processes, and systems for the move to T+1?

The T+1 impact on derivatives documentation is expected to be minimal. ISDA updated and futureproofed’ equity derivative agreements in 2017 at members’ request (replaced hard-coded settlement cycle references with more generic wording). There was limited uptake by market participants of the new protocol at the time as, instead, most chose to amend existing OTC equity documentation on a blockchain basis or otherwise. No change is seen as needed to the master documentation for T+1 at this time. Industry participants should, however, check if payment dates they specify in their confirmations or product descriptions require an update. Also, participants may have to look at updating any specific calendar dates in their Master Confirmation Agreements (MCAs) for products such as equity options (as well as credit default and variance swaps) in several jurisdictions.

Regarding processing:

- There may be risk-booking systems and settlement system updates to make to ensure correct payment timelines are captured and payments can/will be made in the reduced timeframe.

- Market participants also should consider what business day convention applies in the time zones of counterparties.

- Physical- and cash-settled derivatives should be aligned.

While technology solutions are clearly desirable, efforts to identify and implement new systems should not be underestimated. In the meantime, ISDA is working on an operational practice document that should help with some unnecessary problems, for example, those caused by (poor management, communication, and reconfirmation of standing settlement instructions (SSIs) to improve the ability to make payments on a timely basis.

Will ISDA facilitate remediation of legacy trades – transactions outstanding as of May 26, 2024 in Canada/May 27, 2024 in the U.S.?

Yes, ISDA, as it did in the case of the 2017 move to T+2, can facilitate co-ordination (likely two-three months before transition) of what firms expect to do with respect to outstanding (live) transactions executed before May 26/27 2024 and continuing afterward. Firms have not yet begin stating their preferences, and there are various issues to consider, including whether a market participant wants to spend time remediating a transaction that will expire soon versus transactions that will remain on the books for two or three years after. ISDA expects to circulate a table (see attached example) listing equity options, accumulators, and equity/variance swaps/dividend swaps, that members could use to record their own – and better understand other – firms’ intentions regarding the settlement cycle of particular products and business events.

Example of ISDA Table to Capture Approaches to T+1 Transition

| US & CANADA – TRANSITION TO T+1 SETTLEMENT | |||

| Dealer vs Dealer | Settlement cycle for existing trades entered into Prior to [DATE TBC, 2024] | ||

| Event | Scheduled Eq and Funding & Expiry Cash flows (if applicable) | Unwinds / Upzise / (if applicable) | Physical delivery at expiry (if applicable) |

| Equity Swaps | |||

| Single Share | |||

| Indices | |||

| Equity Options | |||

| Single Share | |||

| Indices | |||

| Variance Swaps | |||

| Single Share | |||

| Indices | |||

| Dividend Swaps | |||

| Single Share | |||

| Indices | |||

| Accumulators / Deccumulators | |||

| Single Share | |||

| Indices | |||

| Other | |||

| Single Share | |||

| Indices | |||

| Dealer vs Client | Settlement cycle for existing trades entered into Prior to [DATE TBC, 2024] | ||

| Event | Scheduled Eq and Funding & Expiry Cash flows (if applicable) | Unwinds / Upzise (if applicable) | Physical delivery at expiry (if applicable) |

| Equity Swaps | |||

| Single Share | |||

| Indices | |||

| Equity Options | |||

| Single Share | |||

| Indices | |||

| Variance Swaps | |||

| Single Share | |||

| Indices | |||

| Dividend Swaps | |||

| Single Share | |||

| Indices | |||

| Other | |||

| Single Share | |||

| Indices | |||

| Additional information: | |||

26. Y a-t-il des changements T+1 à à envisager en ce qui concerne des produits dérivés (documentation, traitement, transactions en cours lorsque les ententes chevauchent la date du 27 mai 2024, etc.)? (29 septembre 2023)

Les produits dérivés américains passent-ils à T+1?

Oui, non et peut-être. Si un produit dérivé est admissible à la DTC et non dispensé, il passera à T+1. La section 3(a)(10) du Exchange Act englobe les swaps basés sur des titres et les options, et exclut les titres dispensés (en effet, les swaps basés sur des titres sont dispensés). Advenant qu’un produit dérivé soit dispensé, il pourrait passer à T+1 en vertu d’une entente ou d’une pratique de marché. Par exemple, les options de gré à gré n’ont pas l’obligation de suivre le cycle T+1, mais leur alignement sur les options cotées, passant à T+1, est attendu.

Quels produits dérivés passeront à T+1?

Lors d’une présentation de l’ISDA sur T+1 organisée par la SIFMA, les participants ont appris que règle générale, les sociétés s’attendront à ce que les titres admissibles au dépôt et passés de T+3 à T+2 passent sans doute de T+2 à T+1 dans l’objectif du maintien de flux de trésorerie alignés (évitant une hausse du capital, du préfinancement ou des coûts de crédit) et de la réduction du risque commercial entre l’instrument dérivé et la transaction de couverture correspondante. Le marché de gré à gré procédera ainsi dans l’objectif du maintien de flux de trésorerie aussi alignés que possible et pour éviter le risque de base entre les titres et les instruments dérivés correspondants. Même pour les exceptions formelles à la règle de T+1 (par exemple, les swaps basés sur des titres, exemptés), plusieurs pourraient encore choisir d’adopter le cycle T+1 pour éviter un cycle de règlement non synchronisé.

- Les dérivés d’actions sont susceptibles de subir les effets les plus marqués à T+1, tandis que des catégories comme les dérivés de crédit ne devraient pas être touchées à T+1. D’autres catégories d’actifs seraient plus ou moins affectées et les intervenants du marché devront en discuter davantage. Par exemple, les groupes de travail de l’ISDA sur les actions pourraient se pencher sur les dérivés exotiques/hautement structurés, notamment les types de transactions non linéaires et non standard (comme les options à barrière et les options composées).

- D’autres classes d’actifs subiront de possibles répercussions, notamment lorsqu’un intervenant du marché désire aligner les dates de paiement d’un swap de taux d’intérêt sur le règlement du titre. Pour le dollar américain et les transactions à taux SOFR (Secured Overnight Financing Rate – taux de référence choisi en remplacement du LIBOR $US), l’entente sur les produits dérivés est “composée à terme échu”. Le taux SOFR est publié à T+1, la dernière observation étant faite à la date d’échéance, au moment ou le règlement est dû, mais le montant des intérêts dus ne peut être connu. Fort heureusement, de nouvelles conventions de l’ISDA en matière de retour sur investissement, de décalage d’observation et de clôture, sont en vigueur depuis quelques années. Elles se reflètent dans la documentation sectorielle distribuée et utilisée par le marché. Ces ententes permettent l’observation d’un taux afin que le montant des intérêts soit établi avant la date de règlement, déterminant avec certitude le montant et le moment du règlement à T+1. Les sociétés peuvent également choisir de ne pas modifier l’observation du taux, mais d’appliquer plutôt un délai de règlement au montant flottant, convenu selon le cas.

Des modifications seront-elles apportées à la documentation sur les produits dérivés, aux processus et aux systèmes pour la transition à T+1?

Les effets du cycle T+1 sur la documentation relative aux produits dérivés s’annoncent minimes. En 2017, l’ISDA a mis à jour et a revu, en prévision du futur, les ententes afférentes aux dérivés d’actions à la demande des membres (référence au cycle de règlement encodée remplacée par un libellé générique). L’adoption du nouveau protocole par les intervenants du marché a été limitée à l’époque, la plupart d’entre eux modifiant plutôt la documentation existante sur les actions de gré à gré selon les blocs de chaîne ou autrement. Aucune modification ne doit nécessairement être apportée à la documentation principale pour T+1 présentement. Les participants sectoriels devront, cependant, s’assurer que les dates de règlement inscrites dans leurs confirmations ou descriptions de produits soient mise à jour. Les intervenants devront par ailleurs mettre à jour toute date calendaire particulière apparaissant aux ententes principales de confirmation (EPC) pour des produits comme les options sur actions (ainsi que les swaps de défaut de crédit et de variance) dans plusieurs juridictions.

Au sujet du processus :

- Des mises à jour aux mécanismes de souscription de risques et de systèmes de règlement peuvent se révéler nécessaires afin que les délais de paiement corrects soient pris en considération et que les règlements puissent être effectués et le soient dans les délais raccourcis.

- Les intervenants du marché doivent aussi s’interroger sur les modalités de jour ouvrable s’appliquant aux fuseaux horaires des contreparties.

- Les produits dérivés réglés physiquement et en liquidités doivent faire l’objet d’un alignement.

Les solutions technologiques s’avèrent de toute évidence souhaitables, et il ne faut pas sous-estimer les efforts déployés pour déterminer et mettre en œuvre de nouveaux systèmes. Dans l’intervalle, l’ISDA s’applique à concevoir un document sur les pratiques opérationnelles visant la résolution de certains problèmes inutiles, par exemple les difficultés de mauvaise gestion, de communication et de reconfirmation de consignes permanentes de règlement (CPR) visant à améliorer la capacité de procéder à des paiements en temps utiles).

L’ISDA facilitera-t-elle la correction d’anciennes transactions – les transactions en cours au 26 mai 2024 au Canada et au 27 mai 2024 aux États-Unis?

Oui, l’ISDA, comme ce fut le cas lors de la transition à T+2 de 2017, peut faciliter la coordination (deux ou trois mois avant la transition) des actions de sociétés relativement aux transactions en cours (en direct) exécutées avant les 26 et 27 mai 2024 et se poursuivant. Les sociétés n’ont pas indiqué pour l’instant leurs préférences; plusieurs questions sont à prendre en compte, notamment si un intervenant du marché souhaite se consacrer à corriger une transaction à échéance rapide comparativement à des transactions inscrites dans les livres pour deux ou trois années après. L’ISDA prévoit de publier un tableau (exemple ci-joint) énumérant les options sur actions, les contrats à terme de cumul et les swaps d’actions, les swaps de variance et les swaps de dividendes, à l’intention des membres pour inscrire leurs intentions – et mieux comprendre celles des autres sociétés – au sujet du cycle de règlement de produits et d’événements commerciaux particuliers.

Exemple de tableau de l’ISDA présentant les approches de la transition à T+1

| ÉTATS-UNIS ET CANADA – RÈGLEMENT AVEC LE PASSAGE À T+1 | ||||

| Courtier vs. courtier | Cycle de règlement pou les titres existants inscrits avant le [DATE 2024] | |||

| Événement | Flux de trésorerie prévus pour les capitaux propres, le financement et l’échéance (le cas échéant) | Baisse/Hausse

(le cas échéant) |

Livraison physique à l’échéance

(le cas échéant) |

|

| Swaps sur actions | ||||

| Action individuelle | ||||

| Indices | ||||

| Options sur actions | ||||

| Action individuelle | ||||

| Indices | ||||

| Swaps de variance | ||||

| Action individuelle | ||||

| Indices | ||||

| Swaps sur dividendes | ||||

| Action individuelle | ||||

| Indices | ||||

| Contrats à terme de cumul et décumul | ||||

| Action individuelle | ||||

| Indices | ||||

| Autres | ||||

| Action individuelle | ||||

| Indices | ||||

| Courtier vs. client | Cycle de règlement pour les titres existants inscrits avant [DATE 2024] | |||

| Événement | Flux de trésorerie prévus pour les capitaux propres, le financement et l’échéance

(le cas échéant) |

Baisse/Hausse

(le cas échéant) |

Livraison physique à l’échéance

(le cas échéant) |

|

| Swaps sur actions | ||||

| Action individuelle | ||||

| Indices | ||||

| Options sur actions | ||||

| Action individuelle | ||||

| Indices | ||||

| Swaps de variance | ||||

| Action individuelle | ||||

| Indices | ||||

| Swaps sur dividendes | ||||

| Action individuelle | ||||

| Indices | ||||

| Autres | ||||

| Action individuelle | ||||

| Indices | ||||

| Information supplémentaire : | ||||

25. What types of trades are subject to matching requirements and what are the requirements of NI 24-101? (September 29, 2023)

| Question | Answer |

| 1. What trades are subject to trade matching requirements under NI 24-101 Institutional Trade Matching and Settlement? | Institutional trade matching (“ITM”) trades are trades for institutional client accounts that permit DAP/RAP[1] through CDS, and settlement is completed by a custodian (i.e. other than the dealer executing the trade).

|

| 2. What are the NI 24-101 trade matching requirements for registered dealers and advisers? | They cannot execute/give an order to execute an ITM trade unless they have, maintain and enforce policies and procedures designed to match these trades as soon as practical after the trade is executed and no later than the “established deadline”.[2]

|

| 3. What are the NI 24-101 documentation requirements for registered dealers and advisers? | They cannot open an account for ITM trades or accept an order to execute an ITM trade for an account unless they have policies and procedures to encourage each trade matching party[3] to enter into a trade matching agreement or provide a trade matching statement.

|

| 4. There is an updated Trade Matching Statement (“TMS”) that has been approved by the industry – do we need to obtain new TMS’s from existing clients? | There is a new TMS that has been approved by the CCMA and reviewed and endorsed by CIRO. The TMS is available on both the CCMA[4] and the CIRO[5] websites. For onboarding new clients, the updated TMS should be used.

There is no requirement to obtain an updated TMS from existing clients. Firms should refer to NI 24-101 Institutional Trade Matching and Settlement and Companion Policy 24-101CP Institutional Trade Matching and Settlement for specific compliance obligations and expectations |

| 5. Do registered dealers and advisers have to file exception reports? | NI 24-101 has a requirement that if matched ITM trades (for both value and volume) for a calendar quarter are less than 90% for the “established deadline”, and exception report (including why the required matching was not achieved and the steps to be undertaken to correct) has to be provided to the securities regulatory authorities.

However, there was a 3-year moratorium on this exception reporting commencing July 1, 2020. This moratorium was extended on July 2, 2023 and will end on the earlier of adoption of amendments to NI 24-101 (expected to coincide with the industry’s transition on May 27, 2024) or January 1, 2025. Note that this exception reporting requirement has been proposed to be repealed by the CSA meaning the exception reports would no longer be required.[6] Further note that the CSA has said this does not relieve firms from their other NI 24-101 compliance responsibilities. |

| 6. What reporting must the clearing agency do? | It must deliver reporting to the securities regulatory authorities no later than 30 days after the end of a calendar quarter. The report includes aggregated matching trade statistics calculated as per NI 24-101. CDS also publishes aggregate statistics on its website. |

| 7. What are the settlement requirements under NI 24-101? | Dealers must have and enforce trade settlement policies and procedures so a trade settles as per the standard settlement date established by CIRO or the marketplace on which the trade was executed (unless the counterparties agreed to a different settlement date); otherwise the trade may not be executed.

Canada is moving to T+1 in concert with the United States; CIRO and marketplace rules will be aligned for this transition. |

| 8. Are there any types of trades that are exempted from the trade matching or settlement requirements? | Trades in the following are not subject to the NI 24-101 requirements:

· newly issued securities or for which a prospectus is required to be sent or delivered, · a security to the issuer of the security, · connection with a take-over bid, issuer bid, amalgamation, merger, reorganization, arrangement or similar transaction, · accordance with the terms of conversion, exchange or exercise of a security previously issued by an issuer, · securities lending, repurchase, reverse repurchase or similar financing transactions, · investment funds (purchases governed by Part 9 or redemptions governed by Part 10 of NI 81-102 Investment Funds), · securities to be settled outside Canada, · options, futures, or similar derivative trades, and · negotiable promissory notes, commercial paper or similar short-term debt obligation that, in the normal course, would settle in Canada on T. Note that trades in these securities may settle on a T+1 or shorter basis in any event as per their contractual or other requirements. |

| 9. How do CIRO rules apply in regards to the NI 24-101 requirements? | If an SRO has rules dealing with the same subject matter as the NI 24-101 requirements (and these rules were vetted by the securities regulatory authorities), provided the SRO member complies with the SRO rules, the NI 24-101 requirements will not apply.

As noted in the following, CIRO has rules for broker-to-broker trade matching. NI 24-101 will apply to ITM trades as CIRO does not have ITM rules covering the same subject matter as the NI 24-101 requirements. There are also CIRO requirements for ITM matching with respect to written trade confirmation suppression as described below. |

| 10. Does CIRO have trade matching rules? | Yes. The CIRO rules (named Investment Dealer and Partially Consolidated Rules) have matching requirements for non-exchange trades. These trades are broker-to-broker (i.e. between two dealers), in CDS-eligible securities that have not been submitted to CDS’s CNS service.[7]

For written trade confirmation suppression, CIRO also has requirements for ITM trade matching as described below. |

| 11. What is the CIRO trade matching reporting requirement? | Currently CIRO requires exception reporting (including an action plan to remedy) where a dealer’s broker-to-broker trade matching falls below 90% for a quarter.

The percentage is calculated by dividing the total of a quarter’s compliant trades (excluding “don’t know” trades) by the total of a broker’s non-exchange trades. Trades entered (or accepted) at or before 6:00 p.m. are considered compliant trades. Similar to the proposed repeal of the NI 24-101 quarterly reporting by registered dealers and advisers, CIRO has proposed to repeal the broker-to-broker exception reporting for non-exchange trades where a dealer’s broker-to-broker trade matching falls below 90% for a quarter; however where the dealer’s matching is below 90% for more than two consecutive quarters, CIRO may pursue disciplinary action.[8] CIRO will continue to monitor the statistics it receives from CDS for these trades. |

| 12. How does trade matching impact written confirmations under CIRO rules? | Currently, a dealer does not need to send written trade confirmations to a client with a DAP/RAP account if, for:

· ITM trades, the dealer has a quarterly compliant trade percentage >= 85% for at least two of the last four quarters · broker-to-broker trades, the dealer has been compliant for at least two of the last four quarters, and for any non-compliant reports filed in this period, the quarterly compliant trade percentage has not been less than 85% As noted in Question 11, CIRO has proposed to repeal the requirement to file non-compliant reports for matching falling below 90% in a quarter. Dealers will still be required to maintain a quarterly compliant trade percentage of greater than or equal to 85% for at least two of the last four quarters for both ITM trades and broker-to-broker trades, in order to suppress trade confirmations. |

[1] Delivery Against Payment – Receipt Against Payment

[2] Currently by noon on T+1; CSA staff recommended the CSA approve an amendment to 3:59 a.m. on T+1. https://www.osc.ca/sites/default/files/2023-08/csa_20230810_24-319_update-staff-recommendation.pdf. The industry has agreed to a best practice of ITM trade entry by 7:30 p.m. on T.

[3] Registered advisors, registered dealers, institutional investors, and custodians.

[4] Standardized Trade Matching Statement-NI 24-101 (September 26, 2023; in MS Word)

[5] CIRO Rules Bulletin 23-0141 – National Instrument 24-101 trade-matching statement (with fillable pdf)

[6] https://www.osc.ca/sites/default/files/2023-06/csa_20230615_24-930.pdf.

[7] CIRO Rule subsection 4751(1). Non-exchange trades are “[a]ny trade in a CDS eligible security (excluding new issue trades and repurchase agreement transactions and reverse repurchase agreement transactions) between two Dealer Members, which has not been submitted to the CDS continuous net settlement service by a Marketplace or an acceptable foreign marketplace. A non‐exchange trade includes the dealer to dealer portion of a jitney trade that is executed between two Dealer Members that is not reported by a Marketplace or an acceptable foreign marketplace”

[8] https://www.osc.ca/sites/default/files/2023-04/newsro_20230420_notice.pdf.

25. Quels types de transactions sont soumises à l'obligation d'appariement et quelles sont les exigences de la NC 24-101? (29 septembre 2023)

| Question | Réponse |

| 1. Quelles transactions sont soumises à l’obligation d’appariement en vertu de la Norme canadienne (NC) 24-101 sur l’appariement et le règlement des opérations institutionnelles? | L’appariement des transactions institutionnelles (ATI) désigne une transaction pour un compte client institutionnel qui permet la LCP/RCP[1] par le biais de la CDS, et dont le règlement est effectué par un dépositaire (autre que le courtier qui exécute la transaction).

|

| 2. Quelles sont les exigences de la NC 24-101 en matière d’appariement des transactions pour les courtiers et les conseillers inscrits? | La société ne peut exécuter ni donner l’ordre d’exécuter une transaction ATI à moins d’avoir, de maintenir et d’appliquer des politiques et des procédures conçues pour l’appariement de ces transactions aussitôt que possible après l’exécution de la transaction et au plus tard à la « date limite établie ».[2]

|

| 3. Quelles sont les exigences documentaires de la NC 24-101 pour les courtiers et les conseillers inscrits? | La société ne peut pas ouvrir de compte pour des transactions ATI ni accepter un ordre d’exécution d’une transaction ATI pour un compte, à moins de disposer de politiques et de procédures visant à encourager chaque partie[3] à l’appariement de transactions à conclure une entente d’appariement de transactions ou à fournir une déclaration d’appariement de transactions. |

| 4. Une déclaration d’appariement de transactions (« DAT ») mise à jour a été approuvée par le secteur – devons-nous obtenir de nouvelles DAT de nos clients existants? | Une nouvelle DAT a été approuvée par l’ACMC et examinée et approuvée par l’Organisme canadien de réglementation des investissements (OCRI). La DAT est présentée sur les sites Internet de l’ACMC[4] et l’OCRI[5]. Pour intégrer de nouveaux clients, la DAT mise à jour doit être utilisée.

Une DAT mise à jour n’est pas exigée pour les clients existants. Les sociétés doivent se référer à la NC 24-101 sur l’appariement et le règlement des opérations institutionnelles et l’instruction complémentaire 24-101CP sur l’appariement et le règlement des opérations institutionnelles pour en savoir plus sur les obligations et les attentes spécifiques de conformité. |

| 5. Les courtiers et conseillers inscrits doivent-ils produire des déclarations d’exception? | La NC 24-101 prévoit que si les transactions ATI appariées (en valeur et en volume) pour un trimestre civil sont inférieures à 90 % dans le « délai établi », un rapport d’exception (indiquant les raisons pour lesquelles l’appariement exigé n’a pas été réalisé et les mesures correctives) doit être fourni aux autorités de réglementation des marchés de capitaux.

Cependant, un moratoire de trois ans sur cette déclaration d’exception a été institué au 1er juillet 2020, puis prolongé le 2 juillet 2023 et il prendra fin à la date la plus proche entre l’adoption des modifications de la NC 24-101 (qui devrait coïncider avec la transition sectorielle du 27 mai 2024) et le 1er janvier 2025. À noter d’une part que les ACVM ont proposé d’abroger l’obligation de déclaration d’exception; aussi, les déclarations d’exception ne seraient plus exigées[6]. D’autre part, les ACVM indiquent que les sociétés ne sont pas pour autant libérées de leurs autres responsabilités de conformité à la NC 24-101. |

| 6. Quels rapports doivent être produits par l’organisme de compensation? | L’organisme doit produire un rapport pour les autorités de réglementation au plus tard 30 jours après la fin d’un trimestre civil. Le rapport fait état de statistiques globales sur les transactions appariées calculées conformément à la NC 24-101. La CDS publie également des statistiques globales sur son site Web. |

| 7. Quelles sont les exigences de règlement en vertu de la NC 24-101? | Les courtiers doivent se doter de politiques et des procédures de règlement des transactions et les appliquer de sorte qu’une transaction soit réglée conformément à la date de règlement standard établie par l’OCRI ou le marché sur lequel la transaction a été exécutée (à moins que les parties s’entendent sur une date différente de règlement); autrement, la transaction pourrait ne pas aboutir.

Le Canada passe à T+1 de concert avec les États-Unis; les règles de l’OCRI et des places de marché s’aligneront à cette transition. |

| 8. Quelles catégories de transactions sont exemptées des exigences d’appariement ou de règlement? | Les transactions suivantes ne sont pas soumises aux exigences de la NC 24-101 :

· Les titres nouvellement émis ou pour lesquels un prospectus doit être envoyé ou livré · Un titre à l’émetteur de titre · Une offre publique d’achat, d’une offre publique de rachat, d’une fusion, d’une réorganisation, d’un arrangement ou d’une opération similaire, · Conformité aux conditions de conversion, d’échange ou d’exercice d’un titre précédemment émis par un émetteur · Les transactions de prêt de titres, de mise en pension, de prise en pension ou de financement similaire · Les fonds de placement (achats régis par la partie 9 ou rachats régis par la partie 10 de la NC 81-102 sur les fonds d’investissement) · Les titres devant être réglés à l’étranger · Les options, les contrats à terme ou les transactions similaires sur produits dérivés, et · Les billets à ordre négociables, le papier commercial ou les titres de créance similaires à court terme qui, habituellement, seraient réglés au Canada le jour T. À noter que les transactions sur ces titres se règlent à T+1 ou à une date plus courte, selon les exigences contractuelles ou autres. |

| 9. Les règles de l’OCRI s’appliquent-elles selon les exigences la NC 24-101? | Si un organisme d’autorèglementation (OAR) dispose de règles traitant du même sujet que les exigences de la NC 24-101 (et les autorités de réglementation ont approuvé ces règles), les exigences de la NC 24-101 ne s’appliqueront pas, à condition que le membre de l’OAR se conforme aux règles de l’OAR.

Comme indiqué ci-après, l’OCRI dispose de règles pour l’appariement des transactions de courtier à courtier. La NC 24-101 s’appliquera aux transactions ATI, car l’OCRI ne dispose pas de règles ATI couvrant le même sujet que les exigences de NC 24-101. L’OCRI a également des exigences en matière d’appariement ATI dans le cadre de la suppression de la confirmation écrite de la transaction, comme décrit ci-dessous. |

| 10. L’OCRI dispose-t-il de règles d’appariement de transactions? | Oui. Les règles de l’OCRI (appelées Règles visant les courtiers en placement et règles partiellement consolidées) comportent des exigences d’appariement pour les opérations non boursières. Il s’agit d’opérations de courtier à courtier (c.-à-d. entre deux courtiers) sur des valeurs admissibles à la CDS qui n’ont pas été soumises au service de règlement net continu (RNC) de la CDS.[7]

Pour la suppression des confirmations écrites de transactions, l’OCRI a également des exigences en matière d’appariement des transactions ATI, comme décrit ci-dessous. |

| 11. Qu’est-ce que l’exigence de déclaration de l’appariement des transactions de l’OCRI? | Présentement, l’OCRI exige un rapport d’exception (incluant un plan d’action correctif) lorsque l’appariement des transactions de courtier à courtier est inférieur à 90 % pour un trimestre.

Le pourcentage se calcule en divisant le total des transactions conformes d’un trimestre (excluant les transactions « ne sait pas ») par le total des transactions non boursières d’un courtier. Les transactions saisies (ou acceptées) à 18 h ou auparavant sont considérées comme des transactions conformes. À l’instar de l’abrogation proposée des rapports trimestriels prévus par la NC 24-101 pour les courtiers et les conseillers inscrits, l’OCRI a proposé d’abroger les rapports d’exception de courtier à courtier pour les opérations non boursières lorsque l’appariement institutionnel d’une transaction de courtier à courtier est inférieure à 90 % pour un trimestre donné; cependant, lorsque l’appariement de courtier est inférieur à 90 % pour plus de deux trimestres consécutifs, l’OCRI pourrait exercer une action disciplinaire[8]. L’OCRI poursuivra la surveillance des statistiques reçues de la CDS pour ces opérations.

|

| 12. Comment l’appariement influence-t-il les confirmations écrites selon les règles de l’OCRI? | Présentement, un courtier n’a pas besoin de confirmer par écrit les transactions de client disposant d’un compte LCP/RCP si :

· pour les transactions ATI, le courtier a un pourcentage trimestriel de transactions conformes >= 85 % pour au minimum deux des quatre derniers trimestres · pour les transactions de courtier à courtier, le courtier a été en conformité pour au minimum deux des quatre derniers trimestres, et pour tout rapport non conforme déposé au cours de cette période, le pourcentage trimestriel de transactions conformes n’a pas été inférieur à 85 %. Tel qu’indiqué à la question 11, l’OCRI a proposé d’abroger l’obligation de produire des rapports de non-conformité lorsque l’appariement est inférieur à 90 % lors d’un trimestre donné. Les courtiers seront toujours tenus de maintenir un pourcentage trimestriel d’opérations conformes supérieur ou égal à 85 % pendant au minimum deux des quatre derniers trimestres, tant pour les transactions ATI que pour les transactions de courtier à courtier, aux fins de suppression des confirmations de transactions. |

[1] Livraison contre paiement (LCP) ou réception contre paiement (RCP)

[2] Présentement à midi à T+1; le personnel des ACVM a recommandé que les ACVM approuvent la modification à 3 h 59 le jour T+1. https://lautorite.qc.ca/fileadmin/lautorite/reglementation/valeurs-mobilieres/0-avis-acvm-staff/2023/2023aout10-24-319-avis-acvm-fr.pdf. Le secteur a convenu d’une meilleure pratique de saisie de l’appariement institutionnel des échanges (AIE) à 19 h 30 le jour T.

[3] Conseillers inscrits, courtiers inscrits, investisseurs institutionnels et dépositaires.

[4] Relevé normalisé de l’appariement des opérations (26 septembre 2023; en MS Word)

[5] Bulletin sur les règles 23-0141 de l’OCRI – Déclaration relative à l’appariement des opérations – Norme canadienne 24-101 (avec formulaire PDF à remplir en direct)

[6] https://www.osc.ca/sites/default/files/2023-06/csa_20230615_24-930.pdf.

[7] Paragraphe 4751(1) des Règles relatives aux courtiers en valeurs mobilières et aux sociétés partiellement consolidées. Les opérations non boursières constituent « toute opération sur une valeur admissible à la CDS (excluant les opérations sur nouvelles émissions et les opérations de mise en pension et de prise en pension) entre deux courtiers membres, non soumise au service de règlement net continu de la CDS par un marché ou un marché étranger reconnu ». Une opération non boursière comprend la partie courtier à courtier d’une transaction de jitney exécutée entre deux courtiers membres non déclarée par un marché ou un marché étranger acceptable.

[8] https://www.osc.ca/sites/default/files/2023-04/newsro_20230420_notice.pdf.

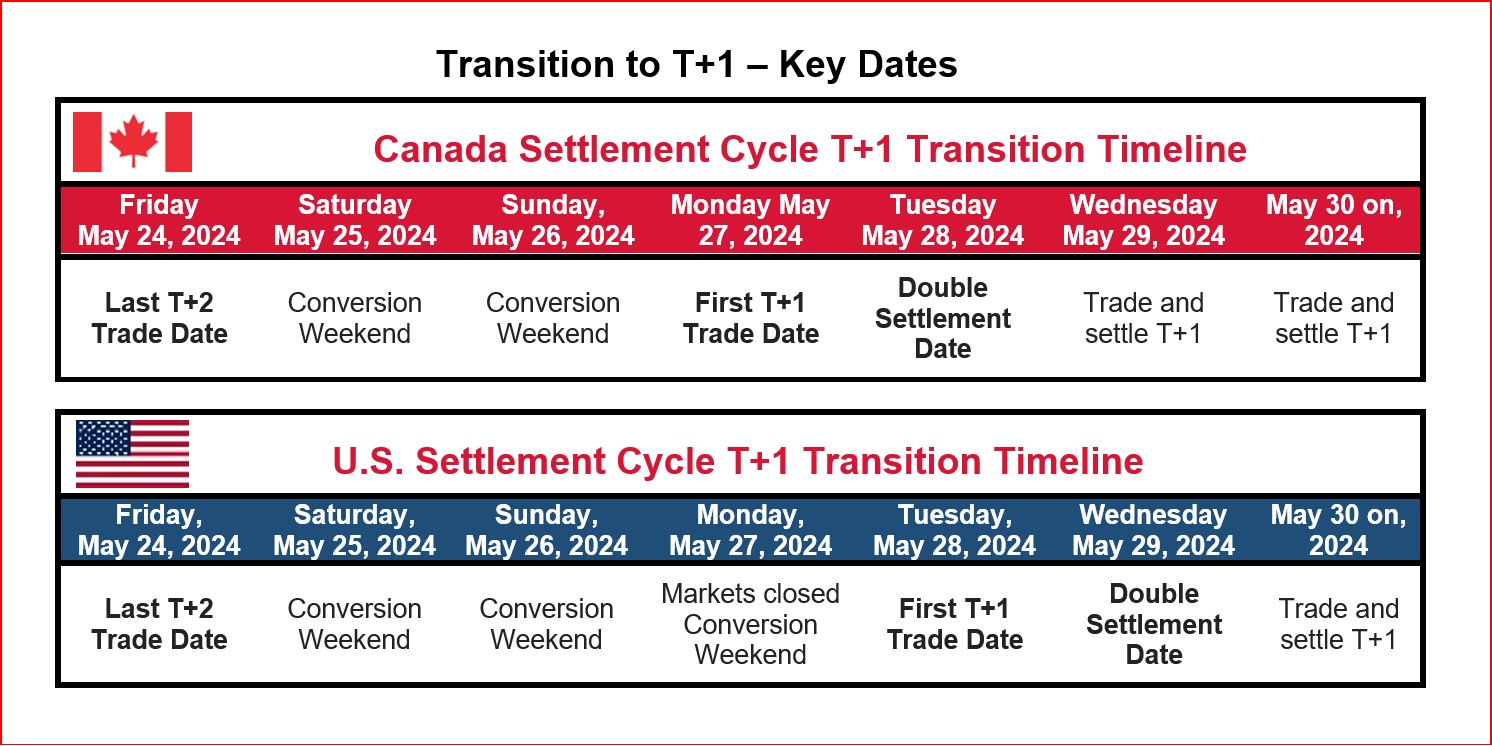

24. What are the key implementation-related days for T+1 and why is the first T+1 trading day for Canada May 27, 2024 - a day earlier than in the U.S.?

When will Canada and the U.S. move to a standard T+1 securities settlement practice?

Canada and the U.S. are transitioning to T+1 at the same time. Capital markets participants in both countries will make systems change to convert to a shortened standard securities settlement cycle – that is, from today’s two days after a trade (or T+2) to the next day (or T+1) – on the May 25/26, 2024 weekend. The last date securities will be traded on the current two-day standard in Canada and the U.S. will be Friday, May 24, 2024. The first day trading on a T+1 basis will be the next business day. In the U.S., the U.S. Securities and Exchange Commission (SEC) mandated Tuesday, May 28, 2024 (after the Memorial Day long weekend) as the transition date and so the first day to trade for next-day settlement. In Canada, securities markets are open on Monday, May 27, 2024, and so Monday will be the first day trades to be settled on a T+1/next-day basis will be transacted in Canada. Trading volumes are historically lower when one market is open and the other is closed.

Most capital markets participants in Canada and the U.S., and some global organizations, had urged the SEC to adopt the Labour Day 2024 weekend – a long weekend in both countries – for a simpler conversion. That said, firms in both markets have extensive experience adapting to situations when one market is closed and the other is open, long weekends can differ throughout the year when Canadian markets may be open and U.S. markets are closed (e.g., the mid-January Martin Luther King Jr. Day); there also are holidays where Canadian markets do not operate (e,g,, Canada Day) while American are open.

What does this mean for market participants?

Below is a table that shows market implications for market participants and investors. The last trades to settle on a T+2 basis in North America will be placed on Friday. Market participants on both sides of the border will transition and test systems conversion on the weekend. The first T+1 trading date and the double settlement date (the settlement of both the last T+2 and the first T+1 trades) will be Monday and Tuesday respectively in Canada and, in the U.S., they will be Tuesday and Wednesday. The two countries will again be on identical trading and settlement cycles from Thursday, May 30, 2024 on.

Why is Canada choosing to move to T+1 on a different day from the U.S.?

If Canada were to transition to T+1 on May 28, 2024, Canadian firms would have to implement T+1 system changes on the night of Monday, May 27, which will not allow enough time to validate changes have been made effectively before trading commences on Tuesday, May 28. Also, Memorial Day is a holiday in the U.S., there will be minimal impact of being out of sync for one day. In fact, Memorial Day has historically been a light trading day in Canada and so Monday, May 27 will provide an additional day to confirm that all systems changes have been effective.

Were other options considered and if so what were they and why were they rejected?

One other alternative was discussed: that Canada treat May 27th as a non-trading, non-settlement day. The following concerns of a number of market participants, and how the concerns were addressed, are as follows:

- A T+1 trading date in Canada but not the U.S. would require product-/situation-specific timing issues to be addressed – while this is correct, the majority were common to all ‘holiday-processing’ dates and so resolvable based on past practice; new ones are being added to the CCMA’s Operations Issue Log to be addressed, with ‘workarounds’ to be identified before implementation.

- For U.S. based firms trading and settling in Canada, additional U.S. staff will be required to work on a holiday – while a valid concern, this was felt to be a lesser issue than the risk of Canadian firms having to rush systems changes overnight on May 27, 2024.

- There would be additional work for the Canadian industry in the very unlikely case there is a need to back out systems changes for any reason – while this is a risk for any project, CCMA members will be working with American counterparts to ensure that, as in the 2017 move from T+3 to T+2, there is an appropriate ‘go-/no-go date multiple weeks before implementation to avoid the need for a last-minute backout.

- Make May 27, 2024 a non-trading/non-settlement day in Canada would affect multiple industry stakeholders, including marketplaces (such as exchanges), the Bank of Canada and other regulators, the Canadian Depository for Securities Ltd., the Canadian Payments Association/Payments Canada, CLS Bank, and possibly other organizations; market participants and investors would also have to know and prepare for a one-time change. There was also a thought that the Victoria Day holiday could be advanced was raised, but this also would require agreement from governments across the country, which would be a challenge to achieve.

In summary, it is the Canadian industry member consensus that Monday, May 27 should be the first day of T+1 trading in 2024 because:

- Trying to have May 27, 2024 declared a non-trading/non-settlement day would be resource-intensive and was highly unlikely to be successful

- Canadian market participants need certainty now so firms can proceed to make change decisions with confidence

- Having to implement T+1 overnight between Monday and Tuesday was considered much more risky

- The few challenges identified will be addressed by CCMA committees well in advance of implementation.

23. Why do Canadian capital markets propose 3:59 a.m. ET on T+1 rather than 9:00 p.m. on trade date for T+1 matching purposes? (added February 10, 2023)

(all times shown are Eastern Time)

Canadian regulators have proposed amendments to National Instrument 24-101 Institutional Trade Matching and Settlement (NI 24-101) that would require 90% of institutional trades to be matched by 9:00 p.m. on trade date (T).[i] The U.S. Securities and Exchange Commission (SEC) has proposed a rule requiring 100% of institutional trade matching (i.e., allocations, confirmations, and affirmations) to be completed by midnight on T,[ii] with the U.S.’s DTCC setting a 9:00 p.m. on T operational deadline for affirmations.[iii] Canadian market participants believe that a 90% matching deadline just prior to 4 a.m. on T+1, still before the next business day settlements starts, is the best option, for several reasons, one being that the SEC’s T+1 rule is not yet final.

The SEC’s proposed deadline for transitioning to T+1, published in February 2022, is Q1 2024 . The U.S. and Canadian industries responded to the SEC’s request for comments last year, strongly recommending six months later – Q3 2024. If the SEC chooses Q1 2024 despite leading industry group requests for Labour Day weekend 2024, the transition effort – much more difficult than previous settlement cycle reductions – becomes significantly more challenging, making the Canadian industry’s call for 3:59 a.m. on T+1 matching cut-off even more important.

Why has the Canadian industry recommended 90% trade matching by 3:59 a.m. on T+1 for regulatory and operational purposes instead of a 9:00 p.m. on T deadline?

This deadline was proposed because it maximizes the flexibility for Canadian capital markets participants across the country, and benefits counterparties operating in non-Canadian time zones. Specifically:

- Custodians and buy-side firms will have more time with a 3:59 a.m. T+1 deadline to affirm trades before the day’s netting settlement processes start at 4:00 a.m. on T+1.

- Sell-side firms will be best able to reduce their collateral requirements and complete settlement.

- Each firm can choose an earlier matching deadline before 3:59 a.m. on T+1 (such as 9:00 p.m. on T).

There are two other important considerations:

- Canada’s processing systems differ from those in the U.S. and, therefore, so do solutions.

- Canada and the U.S. have different regulatory approaches: the proposed U.S. rules apply directly to broker-dealers, custodians, and investment managers, while Canada’s NI 24-101 trade-matching deadlines currently apply directly only to registered firms,[iv] leaving other critical market players outside the regulatory framework.

A unified or at least harmonized approach to deadline regulation is more efficient. Don’t different deadlines in Canada and the U.S. mean Canadian companies dealing in the U.S. must have a different process for each country?

Having different deadlines doesn’t mean firms need two separate processes. Canadian firms can adopt the U.S. operational 9 p.m. matching deadline for both their Canadian and U.S. business if they determine this makes sense for their organizations.

Operational rationalization and automation are important (as recommended in the CCMA/industry’s T+3 to T+2 Post Mortem Report).[v] To facilitate greater automation, CDS is, among other things, replacing its CDSX clearing, settlement, and corporate actions systems as part of its post-trade modernization project (PTM).[vi] With (as of the start of February 2023) a minimum of 12 ½ months and a maximum of 19 months until T+1 implementation, achieving full automation (the best solution) is not possible in light of continued unknowns. The lack of a firm SEC transition date and details, in particular, has meant firms have not been able to devote the necessary attention to T+1 while they work on other regulatory projects with clear implementation dates.

Don’t Canadian firms have to operate until 3:59 a.m. on T+1 if Canadian regulators set that time as a deadline for attaining 90% matching?

NI 24-101 doesn’t prescribe a firm’s hours of operations, or that it must stay open until 3:59 a.m. on T+1, if that is the Canadian deadline, as long as the firm meets the 90% affirmation threshold.

Trade-matching currently requires at least some interaction with internal and external counterparties, so wouldn’t these parties need to be available to resolve issues through to 3:59 a.m. on T+1, demanding more staff to affirm all trades?

There is no requirement for more staff between DTCC’s 9:00 p.m. on T operational deadline and what we believe should be Canada’s 3:59 a.m. on T+1 operational and regulatory cut-off. Indeed, some buy-side firms, have advised their custodian that they have little interest in extending their current workdays. However, a 3:59 a.m. on T+1 deadline allows firms (buy-side, custodian, or sell-side) in European markets to affirm or correct trades at the start of their business day on T+1, and for those in Asian markets to have an extra 3.5 hours towards the end of their business day on T+1 to match or address errors.

Doesn’t a later cut-off time for matching mean less time to fix mistakes?

To meet the 100%-matched-at-midnight U.S. regulatory deadline, DTCC has had to advance its system jobs schedule to 9:00 p.m. on T. In fact, a 3:59 a.m. T+1 deadline gives Canadian firms that need, or may need it, an additional seven hours (from 9:00 p.m. on T to 3:59 a.m. on T+1) to match trades or address issues.

Wouldn’t it be more effective if one organization – CDS – compressed the timeline to achieve affirmation by 9:00 p.m. on T, which also sets us up better for T+0?

First, if the CSA’s proposed 9:00 p.m. on T timeline were adopted, sell-side dealers would need to know all of their buy-side allocations by about 5:00 p.m. so buy-side firms and custodians could affirm trades by 7:30 p.m. for institutional trades to be received by 8:00 p.m. at CDS. It is uncertain whether sell-side firms could meet the 5:00 p.m. deadline on T, and equally uncertain that market players, not subject to Canadian regulation, would make (or be able to make) this change. It would also require a significant processing change in how trades are reported by marketplaces to CDS.

Second, if CDS were to have to further change systems now, project risk would increase for both the T+1 and PTM projects as the timelines of the two already overlap. This could mean CDS would have to change both the CDSX (current) and PTM (future state) systems. It might require dealers, custodians, and service providers to also change internal systems, and to test on both the CDSX and PTM systems, increasing resource demands.

Third, rushing to meet a 9:00 p.m. on T deadline on the premise that it might help achieve T+0 is not a persuasive reason because when T+0 might be mandated, and how T+0 might be interpreted, are as yet unclear. It would be more prudent to discuss further globally automated systems, especially because North America moving to T+1 (or less), when Europe and Asian counterparts remain largely on a T+2 standard settlement basis, has generated issues that have yet to be fully resolved, and any move to T+0 could create a completely different set of issues.

———————

[i] https://www.osc.ca/en/securities-law/instruments-rules-policies/2/24-101/csa-notice-and-request-comment-proposed-amendments-national-instrument-24-101-institutional-trade.

[ii] https://www.govinfo.gov/content/pkg/FR-2022-02-24/pdf/2022-03143.pdf.

[iii] https://www.dtcc.com/-/media/Files/PDFs/T2/T1-Functional-Changes.pdf.

[iv] Dealers and advisers registered under securities legislation in Canada.

[v] https://ccma-acmc.ca/en/wp-content/uploads/T2-Project-Post-Mortem-Report-April-19-2018.pdf.

[vi] https://www.cds.ca/about/post-trade-modernization.

22. Are mutual funds currently settling on a T+2 basis going to move to the standard shorter settlement cycle (T+1) in 2024 with debt, equities, and other securities? (added January 31, 2023)

While exchange-traded and closed-end funds will move to T+1, conventional mutual funds may or may not change to the shorter cycle. CSA Staff Notice 81-335 – Investment Funds Settlement Cycles, published December 15, 2022, explains that: “We are not proposing to amend sections 9.4 and 10.4 of National Instrument 81-102 Investment Funds (NI 81-102) at this time to shorten the settlement cycle [from T+2 to T+1] for primary distributions and redemptions of mutual fund securities. If the standard settlement cycle for listed securities moves from two days to one day in Canada, we are of the view that, where practicable, mutual funds should settle primary distributions and redemptions of their securities on T+1 voluntarily. We think it is important, however, to enable each mutual fund to have flexibility to determine whether a T+1 settlement cycle can work for them. Requiring a T+1 settlement cycle in NI 81-102 would not allow for such flexibility.”

Fund managers with material holdings of securities traded in jurisdictions with longer settlement cycles (e.g., Europe and Asia) want the flexibility to remain at T+2 because the purchase or redemption of securities directly with a fund can cause liquidity issues when there is a settlement date ‘mismatch,’ especially as European and Asian markets close much earlier than North-American ones.

Note: 55,028 (56%) of non-segregated-fund products, and a high percentage of segregated funds processed through Fundserv as at the end of 2022 settled on a T+2 basis. It is not known at this time what percentage of these funds will move from T+2 to T+1, nor is it known when this will be known.

21. How will investment fund dealers know which funds are moving to T+1 and which are staying at T+2 (and will any T+3-settling ones move to T+2?)? (added January 31, 2023)

Fundserv is adopting the same approach used for the successful 2017 transition from T+2 to T+1. Fund companies will send fund set-up (FD) or product update (MD) files to notify Fundserv of those funds whose settlement cycle will be reducing to T+1 in advance of the implementation weekend (between Q1 and Q3 2024; specific date unknown). Dealers able to use these files can import them into their systems. For dealers unable to use FD or MD files, Fundserv will host a spreadsheet of funds that are transitioning to T+1 and these dealers will use the information from the spreadsheet to update their records.

20. If in the past, the standard settlement cycle for mutual funds and non-fund securities was the same, making it easier to switch between products; why may more conventional mutual funds continue to settle on a different basis? (added January 31, 2023)

The settlement cycle of conventional mutual funds and other securities have been in sync for many years, however, they do not need to be on the same cycle, as evident in the U.S. (refer FAQ #16). U.S. mutual fund orders have settled on a T+1 basis for a number of years while debt and equities have required a longer time frame. T+1 settlement of conventional mutual funds in the U.S. is possible because U.S. securities markets are much more liquid than Canada’s. Also, the U.S. has rules (such as higher borrowing limits and permitted inter-fund borrowing) as well as practices (advance notice of major mutual fund orders) to help funds manage liquidity needs.]

19. How will conventional mutual fund clients know which of their funds are moving to T+1 and which are staying at T+2 (will Fundserv’s spreadsheet be available publicly?) (added January 31, 2023)

Note: To be answered at a later date.

18: What difference, if any, will having some funds settling on T+2 and others settling on T+1 make to my mutual funds holdings? What difference will it mean for me if I also hold non-fund securities that may now settle on a different cycle? (added January 31, 2023)

Note: To be answered at a later date.

17. When will CDS release a T+1 white paper, impact assessment, roadmap, and business requirements document? (added September 7, 2022)

There will not be a CDS white paper, impact assessment, or roadmap because Canadian market players have agreed, through the CCMA, that the Canadian capital markets industry must move to T+1 for competitive reasons, or face the negative consequences of arbitrage, additional cost, and greater risk that a longer standard settlement cycle than the U.S. would pose.

To move to a standard settlement cycle of T+1 on the same date as the U.S., CDS worked with the CCMA to arrive at a revised CDS Schedule (approved by the CCMA T+1 Steering Committee on June 28, 2022) and CDS and exchanges have since committed to:

- Receiving batch files on an hourly basis, starting at 11:00 a.m. ET (CDS is meeting quarterly with the TMX and other exchanges/marketplaces in this regard)

- Generating/delivering exchange-trade messages and files back to participants and their service bureaus on an hourly basis intraday

- Receiving reconciliation files by 19:30 on T.

CDS will issue a requirements document once all material CDS-related issues in the CCMA Operations Working Group (OWG) Issue Log have been addressed. For this to happen as rapidly as possible, industry participants must drill down now into trade, allocation, confirmation, and settlement systems and processes to identify, discuss, and address at OWG meetings what prevents trades from being confirmed by the end of trade date. The CCMA would like to see the related issue logs closed in Q3/Q4 2022. CDS also expects to issue a requirements document and test plan in Q4 2022.

16. [replaced - See Q 22] Will the settlement cycle for purchases and redemptions of mutual fund units/shares shorten from T+2 to T+1 in 2024? (added September 7, 2022)

Canadian and U.S. mutual funds have been on different standard settlement cycles for purchases and redemptions of their units/shares for a while, with apparently most U.S. funds settling purchases and redemptions on a T+1 cycle for many years. Most Canadian funds, on the other hand, have settled for decades on the same schedule (currently T+2) as Canadian debt, equity, and exchange-traded products, against which mutual fund investments may compete. The difference between Canadian and U.S. fund settlement cycles has not been, and is not expected to be an issue, because unlike in the case of secondary market trading of debt, equity and exchange-traded products, and particularly securities interlisted on Canadian and U.S. exchanges, Canadian and American mutual funds do not compete. Essentially, Canadian mutual funds are not an investment option in the U.S., nor are U.S. mutual funds an option in Canada. One key issue for the Canadian mutual fund industry in the case of shortening the purchase and redemption settlement cycle to T+1 is that many foreign jurisdictions other than the U.S. are not currently proposing to also move to a T+1 settlement cycle. The settlement cycles of certain types of portfolio securities may be problematic for Canadian funds that hold significant amounts of the types of securities/instruments that will remain at a T+2 or greater settlement cycle (e.g., T+3 in some foreign jurisdictions). With U.S. mutual fund market participants being so much larger than that in Canada, Canadian mutual fund industry representatives have been told that these timing differences are not as problematic for them.

15. Will Canada issue a T+1 Playbook like the U.S.? (added September 7, 2022)

The CCMA is not issuing an equivalent to the U.S.’s T+1 Playbook for several reasons:

- Such a tool is needed in the U.S. because of the proportionally larger volume of capital markets participants, much broader range of service providers and vendors, and greater complexity of some systems and markets, as well as the lead that the U.S. is taking in the move to T+1.

- It is not required in Canada (nor was a Canadian version of the U.S. T+2 Playbook published for the T+2 move) because the Canadian marketplace is quite similar in many ways to the U.S. capital markets and, due to Canada’s comparatively smaller capital markets size, it cannot reasonably go in a direction that differs materially from that of the U.S. The well-designed U.S. T+1 Playbook is therefore useful not just for American industry participants but also for Canadian ones.

- Finally, Canada’s capital markets are more concentrated, with only a handful of large infrastructure providers, custodians, service bureaus, and vendors – many of which also operate in the States – linking all parties in the end-to-end processing chain, and significantly reducing delays and simplifying co-ordination.

We encourage CCMA members to review the U.S. T+1 Playbook and use its workbooks. The CCMA will, as for T+2, provide complementary support where needed: a T+1 schedule that dovetails with the U.S.’s, Canadian checklists and Canada-specific frequently-asked questions (FAQs), as well as other tools.

14. Will there be changes in the calculation of the Canadian ex-date for corporate action events in a T+1 environment? (added September 7, 2022)

Corporate actions relative to exchange-traded securities trade with or without any associated income distribution depending on the corporate action’s record date. The security trades without a dividend on the ex date – the trading day before the date of record in today’s T+2 environment. In a T+1 environment, the ex and record dates will be the same – T+1 – in the U.S. and Canada.

In some cases, an exchange may set a later ex-date, for example, due to challenges with stock or large cash dividends, and the securities will trade with a ‘due bill.’ The U.S. has indicated that for trades with due bills, the ex date will be the same as the due bill redemption date, and Canada will adopt the same practice at the time of T+1 transition.

Also impacted are ‘protect’ or letter-of-guarantee periods for voluntary corporate action event (e.g., rights subscription or tender offer) expiries, which usually align with the standard settlement structure (currently T+2) – investors can purchase securities even on the offer’s expiration date, with the protect feature “covered” once the securities settle in two days’ time. In a T+1 settlement cycle, the cover/protect or letter-of-guarantee period will be the expiration date plus one (1) trading day.

There will be a CDS external procedure change requiring regulatory non-disapproval, but no system or rule changes required for CDS.